- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- NCERT (Recorded 500+ Hours)

- Polity Recorded Course

- Geography Recorded Course

- Economy Recorded Course

- AMAC Recorded Course

- Modern India, Post Independence & World History

- Environment Recoded Course

- Governance Recoded Course

- Science & Tech. Recoded Course

- International Relations and Internal Security Recorded Course

- Disaster Management Module Course

- Ethics Recoded Course

- Current Affairs Recoded Course

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

KARNATAKA'S TEMPLE TAX BILL

KARNATAKA'S TEMPLE TAX BILL

The Karnataka Hindu Religious Institutions and Charitable Endowments (Amendment) Bill, 2024, passed in both the State Legislative Assembly and Council. It now awaits approval from the Governor.

- The Bill aims to amend provisions in the Karnataka Hindu Religious Institutions and Charitable Endowments Act (KHRI& CE), 1997.

Historical Background of State Regulation of Temples

- The British government's Religious Endowments Act of 1863 aimed to secularize temple management by transferring control to local committees.

- In 1927, the Justice Party enacted the Madras Hindu Religious Endowments Act, one of the earliest efforts by an elected government to regulate temples.

- The Law Commission of India recommended legislation in 1950 to prevent misuse of temple funds, leading to the enactment of The Tamil Nadu Hindu Religious and Charitable Endowments (TN HR&CE) Act, 1951.

- This act established the Department of Hindu Religious and Charitable Endowments to administer, protect, and preserve temples and their properties.

- The TN HR&CE Act faced a constitutional challenge before the Supreme Court in the Shirur Mutt case (1954). While the court upheld the law but it struck down some provisions.

- A revised TN HR&CE Act was passed in 1959 to address the court's concerns.

Key Highlights of the Bill

-

Alteration of Taxation System

- The Bill aims to change the taxation rules for Hindu temples.

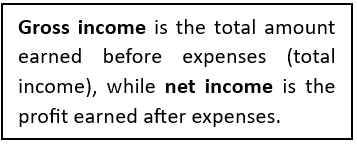

- It proposes diverting 10% of gross income from temples earning over Rs 1 crore annually to a common pool for temple maintenance.

- Previously, 10% of net income was allocated for temples earning over Rs 10 lakh annually.

- Additionally, the Bill suggests allocating 5% of income from temples earning between Rs 10 lakh and Rs 1 crore to the common pool.

- These changes would generate an extra Rs 60 crore from 87 temples with incomes over Rs 1 crore and 311 temples with income exceeding Rs 10 lakh.

-

Utilisation of Common Fund

- The common fund can be used for religious studies, temple maintenance, and charity.

- The common fund pool was created in 2011 through amendments to the 1997 Act.

-

Composition of Committee of Management

- The bill proposed the addition of a member skilled in Vishwakarma Hindu temple architecture and sculpture to the temple "committee of management."

- Temples and religious institutions are required to form a nine-member ‘committee of management.’

- It includes a priest, a member of Scheduled Caste or Scheduled Tribe, two women, and a local member, as per Section 25 of the KHRI& CE 1997 Act.

-

Rajya Dharmika Parishat

- It empowered the Rajya Dharmika Parishat to appoint committee chairpersons and resolve religious disputes, manage temple affairs, and appoint trustees.

- Mandated (authorize) the formation of district and state committees to oversee infrastructure projects for temples with annual earnings exceeding Rs 25 lakh.

Management of Religious Institutions in India

-

Places of Worship Act, 1991

- Enacted to maintain the status of religious places as they were on August 15, 1947.

- Prohibits conversion of places of worship and ensures their religious character.

- Excludes (leaves) ancient monuments governed by the Ancient Monuments and Archaeological Sites and Remains Act, 1958.

-

Constitution of India

- Article 26 grants religious groups the right to establish and manage institutions for religious and charitable purposes.

- Allows them to manage their religious affairs and administer property.

- Muslims, Christians, Sikhs, and others use these rights to manage their institutions.

-

Shiromani Gurdwara Parbandhak Committee (SGPC)

- Manages Sikh Gurdwaras in India and abroad.

- Elected directly by Sikh voters above 18 years old, registered under the Sikh Gurdwaras Act, 1925.

-

Waqf Act of 1954

- Established the Central Waqf Council advising the Central Government on waqf administration.

- State Waqf Boards oversee mosques, graveyards, and religious waqfs.

- Ensures proper management and utilization of waqf properties and revenue.

- Waqf refers to the permanent dedication of properties for religious or charitable purposes recognized by Muslim Law.

Temple Revenue Management in Different States

-

Telangana's Approach

- Telangana's system is similar to Karnataka's, creating a ‘Common Good Fund’ under Section 70 of the Telangana Charitable and Hindu Religious Institutions and Endowments Act, 1987.

- Temples earning over Rs 50,000 annually must give 1.5% of their income to the state government.

- These funds are used for temple maintenance, renovations, religious schools, and building new temples.

-

Kerala's System

- Kerala manages temples mainly through state-run Devaswom (temple) Boards.

- The state has five autonomous Devswom Boards overseeing 3,000+ temples, with board members usually chosen by the ruling government.

- Each board gets a budget from the state government and isn't required to disclose revenue figures.

Must Check: Best IAS Coaching In Delhi

Japan’s New AI Law: Promoting Innovation

Kerala High Court Allows Trans Couple as "Parents" on Birth Certificates

India Opens Doors to Foreign Law Firms

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.