- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- Answer Alpha: Mains 2025 Mentorship

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- Polity

- Geography

- Economy

- Ancient, Medieval and Art & Culture AMAC

- Modern India, Post Independence & World History

- Environment

- Governance

- Science & Technology

- International Relations and Internal Security

- Disaster Management

- Ethics

- NCERT Current Affairs

- Indian Society and Social Issue

- NCERT- Science and Technology

- NCERT - Geography

- NCERT - Ancient History

- NCERT- World History

- NCERT Modern History

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

FINANCIAL DEVOLUTION AMONG STATES

FINANCIAL DEVOLUTION AMONG STATES

26-02-2024

- Several Indian states, especially from South India, claim they aren't receiving their fair share under the current tax devolution scheme.

- They argue that they contribute more to the national tax pool than what they receive.

Devolution of Powers in India

- In India, power is divided between the central government and the states, following a federal system as per the Constitution.

- Devolution means transferring financial resources and decision-making powers from the central government to the states and local governments.

- The Constitution's 7th Schedule outlines the Union List, State List, and Concurrent List, specifying powers of central and state governments.

- Parts V and VI of the Constitution distribute executive powers between the Union and State governments.

- Part VIII details executive powers and functions for union territories.

- The 73rd and 74th Constitutional Amendment Acts of 1992 establish panchayats and municipalities, devolving (transfer) powers and finances to local governments.

-

Tax Devolution in India

- Constitutional provisions: Article 270 of the Constitution outlines the distribution of net tax proceeds between the Union government and the States.

- Statutory laws: Acts like PESA and Forest Rights Act ensure power decentralization to tribal communities.

- PESA stands for Panchayats Extension to Scheduled Areas Act, which was introduced in 1996. The act extends the provisions of Panchayats to the Fifth Schedule Areas (areas with a large tribal population).

- The act's main objectives are to have village governance with participatory democracy and to make the Gram Sabha a nucleus of all activities.

- The Forest Rights Act (FRA) of 2006 recognizes the rights of traditional forest dwellers (resident) and forest dwelling tribal communities to forest resources.

- The FRA was meant to address the historical injustices done to traditional forest dwellers of India.

- Fiscal decentralization: The Finance Commission (FC), appointed every five years, suggests how funds from the central government's tax pool should be divided among states.

- Taxes shared include corporation tax, personal income tax, Central GST, and the Centre's portion of Integrated Goods and Services Tax (IGST).

- Additionally, it provides a formula for distributing funds among individual states.

- States also receive grants-in-aid based on FC recommendations. They are payments in the nature of assistance, donations or contributions made by the Union Government to State Governments.

- Notably, cess and surcharge imposed by the Centre are not part of the divisible pool.

- The 16th Finance Commission, chaired by Dr. Arvind Panagariya, is tasked with making recommendations for 2026-31.

- FC comprises a chairman and four other members appointed by the President.

-

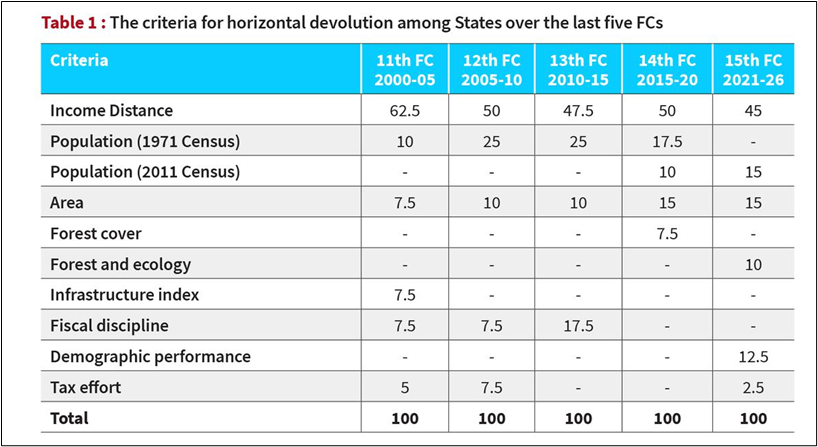

Basis for Allocation

- Vertical Devolution: States receive 41% of the divisible pool according to the 15th FC's recommendation.

- Horizontal Devolution: Allocation among States is based on different criteria.

- Criteria for Horizontal Devolution:

- Income Distance: Measures a state’s income compared to the highest per capita income State i.e. Haryana. States with lower income get a higher share for fairness.

- Population: Based on the 2011 Census. Earlier, it was according to the 1971 Census, but this changed with the 15th FC.

- Forest and Ecology: Considers each State's share of dense forest compared to all States combined.

- Demographic Performance: Recognizes States' efforts in population control. States with lower fertility rates score higher.

- Tax Effort: Rewards States with efficient tax collection efficiency.

-

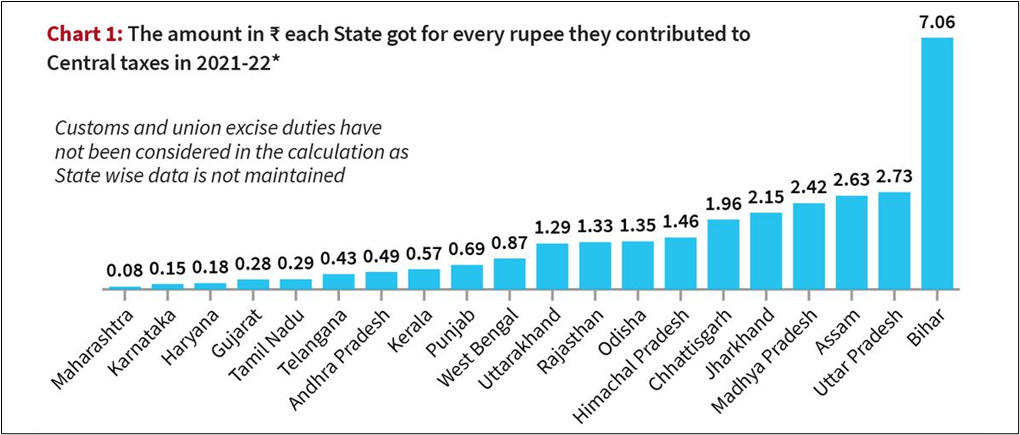

States Contribution Versus Devolution:

-

Challenges in Tax Devolution and solutions:

Challenges in Tax Devolution |

Solutions |

About 23% of the Union government's gross tax receipts for 2024-25 come from cess and surcharge which is not shared with States. |

Enlarging the divisible pool by including some portion of cess and surcharge in the divisible pool and gradually discontinuing them to rationalize tax slabs. |

Industrially developed States receive less than a rupee for every rupee contributed to Central taxes, unlike states like Uttar Pradesh and Bihar. |

Establishing a formal arrangement for State participation in the constitution and workings of the Finance Commission, similar to the GST council. |

Southern States' share in the divisible tax pool has decreased due to emphasis on equity and needs over efficiency in the last six Finance Commissions. |

Increasing efficiency criteria by giving more weightage to efficiency criteria in horizontal devolution, with State GST contribution as a criterion. |

Grants-in-aid vary among states, including revenue deficit, sector-specific, and State-specific grants, as well as grants to local bodies based on population and area. |

Adding more performance indicators like good governance, transparency, and development outcomes could incentivize responsible resource management. |

Must Check: Best IAS Coaching In Delhi

India Climbs SDG Ranks

China's New Trilateral Moves in South Asia

Semaglutide and Tirzepatide

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.