- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- Answer Alpha: Mains 2025 Mentorship

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- Polity

- Geography

- Economy

- Ancient, Medieval and Art & Culture AMAC

- Modern India, Post Independence & World History

- Environment

- Governance

- Science & Technology

- International Relations and Internal Security

- Disaster Management

- Ethics

- NCERT Current Affairs

- Indian Society and Social Issue

- NCERT- Science and Technology

- NCERT - Geography

- NCERT - Ancient History

- NCERT- World History

- NCERT Modern History

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

Effects of liberalization on Indian economy

Effects of liberalization on Indian economy

Effects of liberalization on Indian economy

Definition

-

Economic liberalization is the process of reducing or eliminating government restrictions on business and commerce.

-

Proponents of free markets and free trade, also known as supporters of economic liberalism, are typically those who advance it.

-

As a result of economic liberalization, taxes, social security contributions, and unemployment benefits frequently decrease.

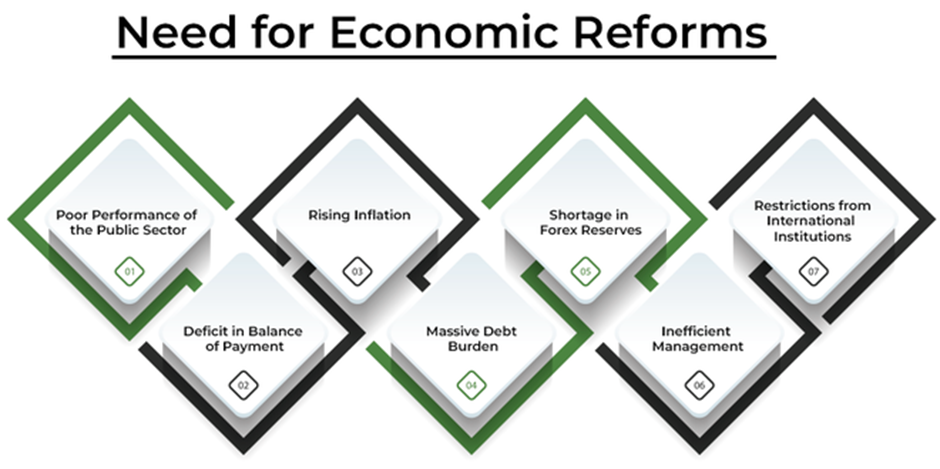

When did financial reforms start in India?

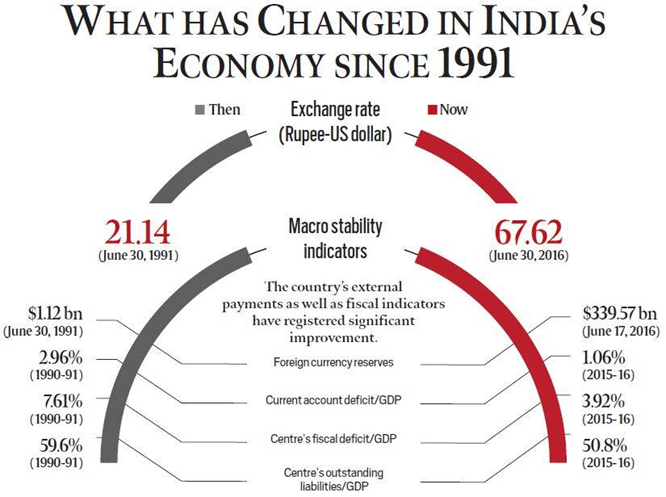

India started a grouping of monetary changes on July 23, 1991, because of a financial and balance-of-payment (BoP) emergency. In the years to come, the historic reforms would fundamentally alter the economy's character and structure.

The BoP crisis was brought on by numerous factors:

-

Fiscal Shortfall: In 1990 and 1991, the fiscal deficit was approximately 8.4% of GDP.

-

1991 Gulf War: The situation was made worse in 1990 and 1991 when Iraq's invasion of Kuwait caused the price of oil to rise.

-

High inflation: The country's economic situation deteriorated as a result of a rapid increase in the money supply, which caused the inflation rate to rise from 6.7% to 16.7%.

This led the government to announce New Economic Policy, 1991 which paved the way for economic reforms in form of LPG reforms. The LPG model allowed for a wide range of reforms, including:

-

Industrial Policy Liberalization: reductions in import tariffs, the elimination of industrial license-permits raj, and other things

-

Start of Privatization: Market deregulation, banking reform, and other things

-

Globalisation: Changing the exchange rate, opening up trade and foreign direct investment policies, getting rid of mandatory convertibility, etc.

Liberalization's goals are to encourage private Indian businesses and multinational corporations to participate.

-

to make it possible for the Indian economy to become global.

-

In order to boost exports, encourage the nation's foreign trade.

-

to find a solution to India's problem with its balance of payments.

-

to increase private sector involvement in India's economic expansion.

-

to increase direct investment from abroad in the Indian industry.

-

to promote competition between domestic businesses.

Policies of Liberalization

The liberalization policies which contributed to the expansion of the economy were: Reforms to the financial sector, the industrial sector, the external sector, the foreign exchange sector, and trade and investment policy reforms are all examples of deregulation.

Impact of Liberalisation

-

Increased Economic Growth: The LPG reforms helped in increasing the rate of economic growth in India. From 1991 to 2020, India's GDP grew at an average rate of 6.7%, compared to an average rate of 3.5% in the previous three decades.

-

Higher Foreign Investment: The LPG reforms opened up several sectors of the Indian economy to foreign investment, leading to an increase in foreign direct investment (FDI) inflows. According to the Ministry of Commerce and Industry, FDI inflows into India increased from $98 million in 1990-91 to $81.72 billion in 2020-21.

-

Improvement in Industrial Productivity: The LPG reforms led to the removal of many restrictions on the private sector, which helped in improving the productivity of industries. According to a study by the Reserve Bank of India, the productivity of the Indian manufacturing sector increased by 6.8% annually between 1991 and 2006.

-

Expansion of the Services Sector: The LPG reforms led to the growth of the services sector in India, which became a major contributor to the country's GDP. According to the Ministry of Statistics and Programme Implementation, the services sector's contribution to India's GDP increased from 37.2% in 1990-91 to 54.3% in 2020-21.

-

Increase in Consumerism: The LPG reforms led to an increase in consumerism in India, as people had access to a wider range of goods and services. According to a study by the National Sample Survey Office, the average monthly per capita expenditure of Indian households increased from Rs. 206 in 1987-88 to Rs. 2,446 in 2017-18.

Negative impacts

-

Widening income inequality: According to the World Inequality Database, the top 1% of India's population held 22% of the country's wealth in 1991, which increased to 42.5% in 2018. In contrast, the bottom 50% of the population's share of wealth decreased from 14% in 1991 to 12.5% in 2018. This suggests that the LPG reforms led to a significant increase in income inequality in India.

-

Job losses: The Economic Survey of India 2020-21 reported that the unemployment rate in India increased from 3.4% in 2017-18 to 6.1% in 2018-19. This increase was attributed to the slow growth in the manufacturing sector, which was affected by the LPG reforms.

-

Increased poverty: According to the World Bank, the poverty rate in India decreased from 36% in 1993 to 9.2% in 2011. However, the rate of poverty reduction slowed down after 2004, with the poverty rate remaining stagnant at around 22%. This suggests that the LPG reforms may have contributed to an increase in poverty in India.

-

Environmental degradation: According to the Environmental Performance Index, India ranked 177th out of 180 countries in terms of air quality in 2020. This suggests that the industrialization and increased economic growth resulting from the LPG reforms may have contributed to increased pollution levels in India.

-

Dependence on foreign investment: According to the Reserve Bank of India, foreign direct investment (FDI) inflows into India increased from $129 million in 1991 to $81.72 billion in 2020. This suggests that the LPG reforms led to an increased dependence on foreign investment in India's economy. However, this also made the Indian economy more vulnerable to global economic fluctuations, as foreign investors could easily pull out their investments.

Need for Economic Reforms 2.0

Once again, the development engine of economic growth in India has started sputtering from the early 2010s with the COVID-19 pandemic further aggravating the slowdown. The slowdown is broad-based across all the sectors - agriculture, industry, and services.

India's goal of becoming a $5 trillion economy by 2025 requires significant economic reforms.

Some of the key reforms, along with relevant data, that can help achieve this goal:

-

Simplify and streamline the tax system: India's tax system is complex, and there are multiple taxes and exemptions that make compliance difficult. Simplifying the tax system can increase compliance and revenue. According to the World Bank's Ease of Doing Business Report 2022, India ranks 115 out of 190 countries in the ease of paying taxes.

-

Boost manufacturing: Manufacturing is a critical sector for India's economic growth. However, India's manufacturing sector has not kept pace with other major economies. According to the United Nations Conference on Trade and Development (UNCTAD), India's manufacturing sector accounted for only 15% of GDP in 2019, compared to 27% in China and 19% in Indonesia.

-

Increase foreign investment: Foreign investment can help drive economic growth in India. However, India has historically been less attractive to foreign investors due to complex regulations and bureaucratic red tape. According to the United Nations Conference on Trade and Development (UNCTAD), India received $64 billion in foreign direct investment (FDI) in 2019, compared to $140 billion in China.

-

Encourage entrepreneurship: India has a large number of entrepreneurs, but they face significant challenges in starting and growing businesses. According to the Global Entrepreneurship Index 2021, India ranks 73rd out of 137 countries in terms of the quality of its entrepreneurship ecosystem.

-

Increase agricultural productivity: Agriculture is a major sector of the Indian economy, but it has suffered from low productivity and poor infrastructure. According to the World Bank, agricultural productivity in India is only 30-50% of its potential.

-

Improve infrastructure: India's infrastructure is inadequate to support economic growth. According to the World Economic Forum's Global Competitiveness Index 2021, India ranks 72nd out of 140 countries in terms of infrastructure quality.

-

Invest in education and skills: India's education system is not producing a workforce with the necessary skills to support economic growth. According to the World Economic Forum's Human Capital Index 2020, India ranks 116th out of 174 countries in terms of the quality of its human capital.

-

Promote exports: Exports can help drive economic growth by increasing foreign exchange earnings. However, India's exports have been relatively stagnant. According to the World Bank, India's exports as a percentage of GDP were 19.7% in 2020, compared to 39.4% in China and 24.9% in Indonesia.

Target of $5 trillion Economy by 2025

The $5 trillion economy target is an ambitious goal set by the Government of India to increase the size of the Indian economy to $5 trillion by 2025. This target was announced by Prime Minister Narendra Modi in 2019 and is part of the government's long-term economic vision for the country.

Achieving a $5 trillion economy would require India's GDP to grow at an average rate of 8% per year over the next few years. This would be a significant increase from the current GDP of around $2.8 trillion (as of 2021).

To achieve this target, the government has identified several key areas of focus, including:

-

Infrastructure development: The government has planned massive investments in infrastructure, including roads, railways, airports, ports, and urban development. This is aimed at creating more jobs, attracting foreign investment, and improving the overall productivity of the economy.

-

Digital transformation: The government aims to promote digital transformation across all sectors of the economy, including agriculture, education, health, and finance. This is expected to drive innovation, increase efficiency, and create new business opportunities.

-

Skill development: The government has launched several programs aimed at skilling the youth and creating a more skilled workforce. This is aimed at boosting productivity and competitiveness of the economy.

-

Promoting entrepreneurship: The government is promoting entrepreneurship by providing access to funding, mentorship, and other resources. This is aimed at creating new business opportunities and promoting innovation.

-

Improving the ease of doing business: The government has taken several measures to improve the ease of doing business in India, including simplifying regulations, reducing bureaucratic hurdles, and streamlining processes. This is aimed at attracting more foreign investment and boosting the overall productivity of the economy.

Schemes launched by Government

The Government of India has implemented several major economic programs over the years, aimed at promoting economic growth, development, and social welfare.

Some of the major economic programs of the Government of India are:

-

Make in India: Launched in 2014, this program aims to promote manufacturing in India and attract foreign investment in the sector. It seeks to create jobs, boost entrepreneurship, and increase the share of manufacturing in GDP.

-

Digital India: Launched in 2015, this program aims to transform India into a digitally empowered society and knowledge economy. It seeks to provide digital infrastructure, digital literacy, and digital services to citizens across the country.

-

Skill India: Launched in 2015, this program aims to provide skill training and vocational education to youth across the country. It seeks to create a skilled workforce that can meet the demands of the industry and contribute to the economy.

-

Pradhan Mantri Jan Dhan Yojana: Launched in 2014, this program aims to provide financial inclusion to the unbanked population of the country. It seeks to provide access to banking services, insurance, and pension schemes to all citizens.

-

Atmanirbhar Bharat Abhiyan: Launched in 2020, this program aims to promote self-reliance and self-sufficiency in various sectors of the economy. It seeks to boost domestic production, reduce dependence on imports, and create jobs and opportunities for the youth.

While achieving the $5 trillion economy target is a challenging task, the government is working towards it by implementing several reforms and measures aimed at boosting economic growth and development in the country.

Must Check: Best IAS Coaching Institute In Delhi

Donald Trump’s Strategic Bitcoin Reserve Executive Order

Navratna Status For IRCTC And IRFC

FINANCE ACT 2025

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.