- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- Answer Alpha: Mains 2025 Mentorship

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- NCERT- First Ladder

- Polity

- Geography

- Economy

- Ancient, Medieval and Art & Culture AMAC

- Modern India, Post Independence & World History

- Environment

- Governance

- Science & Technology

- International Relations and Internal Security

- Disaster Management

- Ethics

- Current Affairs

- Indian Society and Social Issue

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

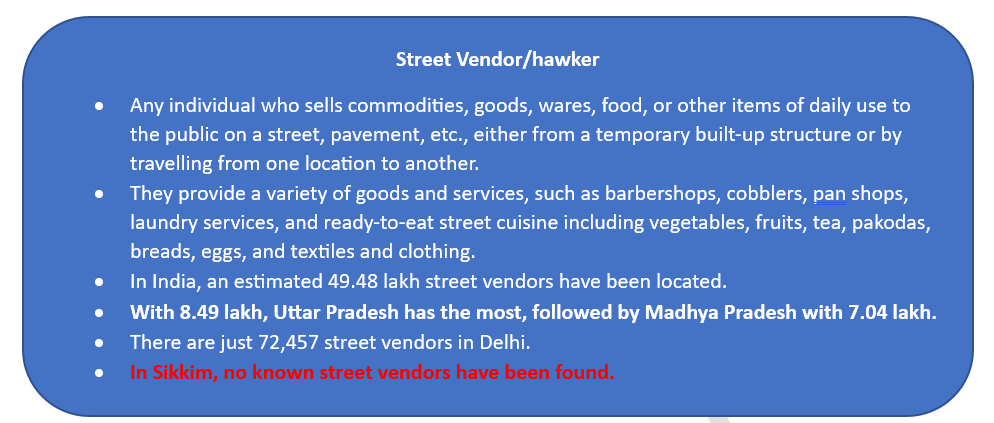

PM-SVANidhi

PM-SVANidhi

Latest Context

In the three years after the Prime Minister Street Vendor's AtmaNirbhar Nidhi (PM-SVANidhi) was introduced on June 1, 2020, more than 46.54 lakh small working capital loans have been given to street vendors.

- 46,54,302 loans in total had been disbursed. About 40% of such loans (18,50,987) have already been returned.

Key Features of the PM-SVANidhi

- It is a Central Sector Scheme, which means that the Ministry of Housing and Urban Affairs entirely funds it, and has the following objectives:

- To facilitate working capital loan.

- To incentivize regular repayment.

- To reward digital transactions.

- Additional to the first and second loans of 10,000 and 20,000 each, a third term loan of up to 50,000 is introduced.

- Loans would be without collateral.

Lending Agencies:

- Due of their proximity and ground-level presence among the urban poor, including street vendors, microfinance institutions, non-banking financial companies, and self-help groups have been permitted.

Eligibility:

- Only those States and UTs that have published their rules and scheme under the 2014 Street Vendors (Protection of Livelihood and Regulation of Street Vending) Act are eligible for the programme.

- However, participants from Meghalaya, which has its own State Street Vendors Act, are allowed.

Street Vendors:

- All street vendors operating in urban areas are eligible for the Scheme.

- Previously, the Scheme was open to all street vendors who planned to start selling on or before March 24, 2020.

Benefits of Early Repayment:

- Interest Subsidy: Beneficiaries' bank accounts will be credited with a 7% annual interest subsidy upon timely/early loan repayment via direct benefit transfer on a six-monthly basis.

- Credit Limits Extension: The scheme allows for an increase in credit limit upon timely/early loan repayment; hence, if a street vendor pays his or her installments on time or earlier, he or she can build credit and become qualified for a larger term loan.

- No-Penalty on Early Repayment:

- There won't be any penalties for paying back the loan early.

- A loan or debt is cleared ahead of schedule by early repayment (also known as resettlement).

- For early loan repayment, many banks and lenders impose penalties.

E-governance:

- Encourage Digital Transactions: Through monthly cash back, the scheme encourages street vendors to do digital transactions.

- Transparency:

- A digital platform with a web portal and mobile app is being built to manage the programme with an end-to-end solution, in keeping with the objective of using technology to ensure effective delivery and transparency.

- This platform would combine the UdyamiMitra portal of SIDBI for credit administration with the PAiSA portal of MoHUA for automatically administering interest subsidies.

- Financial Inclusion: It helps in integrating the vendors into the formal financial system.

Focus on Capacity Building:

- A nationwide programme for information, education, and communication (IEC) initiatives will be launched by the MoHUA in cooperation with State Governments to enhance the capacities of all stakeholders and promote financial literacy.

Role of Urban Local Bodies (ULBs):

- ULBs will be crucial in the scheme's execution since they will make sure to identify the recipient and effectively reach out to them.

Q. Can the vicious cycle of gender inequality, poverty and malnutrition be broken through microfinancing of women SHGs? Explain with examples. (2021)

Q. How has globalization led to the reduction of employment in the formal sector of the Indian economy? Is increased informalization detrimental to the development of the country? (2016)

Must Check: Best IAS Coaching Centre In Delhi

First-Ever Image of Sun’s South Pole Captured

Six Areas to Get New Air Quality Monitoring

Rising Tensions: The Iran-Israel Crisis

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.