- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- Answer Alpha: Mains 2025 Mentorship

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- Polity

- Geography

- Economy

- Ancient, Medieval and Art & Culture AMAC

- Modern India, Post Independence & World History

- Environment

- Governance

- Science & Technology

- International Relations and Internal Security

- Disaster Management

- Ethics

- NCERT Current Affairs

- Indian Society and Social Issue

- NCERT- Science and Technology

- NCERT - Geography

- NCERT - Ancient History

- NCERT- World History

- NCERT Modern History

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

PayU Gets Approval as Payment Aggregator

PayU Gets Approval as Payment Aggregator

Fintech firm PayU recently announced that it has received in-principle approval from the Reserve Bank of India (RBI) to operate as a payment aggregator (PA) under the Payment and Settlement Systems (PSS) Act, 2007.

- In-principle approval from RBI allows PayU to onboard new merchants, yet final approval usually takes 6 months to a year.

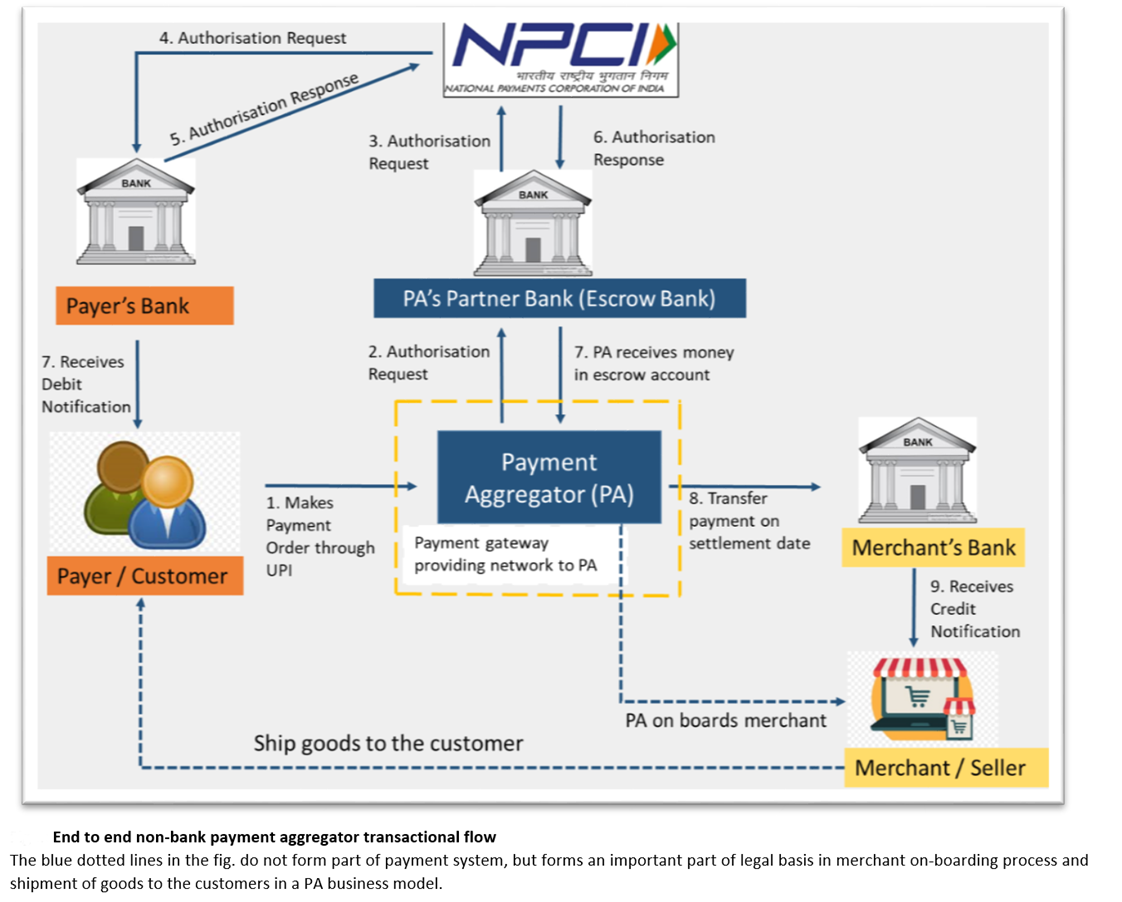

About Payment Aggregators:

- PAs serve as intermediaries between businesses and financial institutions, handling payment processing on behalf of merchants.

- They simplify the process of accepting electronic payments and streamline the payment acceptance process, eliminating the need for businesses to establish direct relationships with financial entities.

- PAs enable businesses to accept various payment methods, including credit cards, debit cards, e-wallets, and bank transfers, through a single platform.

- Examples of PAs include Google Pay, Amazon Pay, Phone pe, and PayPal.

Capital Requirements for PAs:

- New PAs must meet specific capital requirements set by the Reserve Bank of India (RBI).

- At the time of application, PAs must have a minimum net worth of Rs. 15 crore, which must reach Rs. 25 crore by the end of the third financial year following authorization.

Authorisation Process for PAs:

- Banks providing PA services as part of their banking relationships do not require separate authorization.

- However, non-bank PAs must obtain authorization from the RBI under the Payment and Settlement Systems Act, 2007 (PSS).

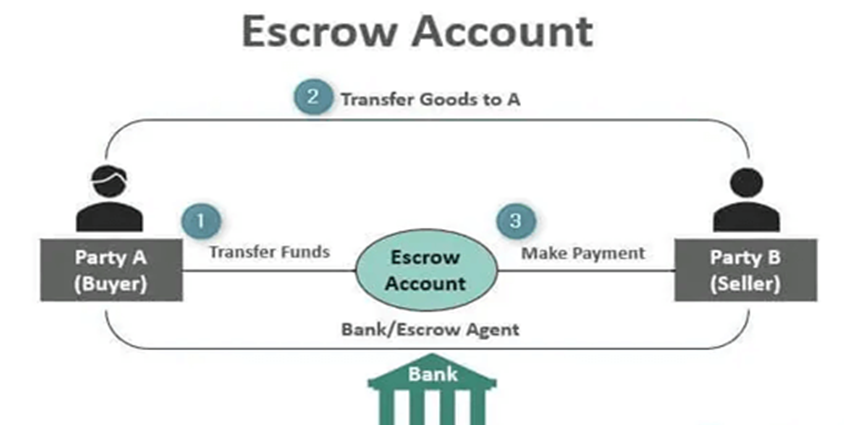

Settlement and Escrow Account Management:

- Non-bank PAs are required to maintain funds collected in an escrow account with a scheduled commercial bank.

PAs must adhere to specific timelines for settling funds with merchants based on the transaction lifecycle and agreed-upon terms.

Note:

- Unlike PAs, Payment Gateways (PGs) offer technological infrastructure to facilitate and route the processing of online payment transactions without managing the funds.

- On the other hand, Payment Aggregators allow merchants to provide multiple payment options on their platforms, including the features of a payment gateway.

|

Basis of Distinction |

Payment Gateway |

Payment Aggregator |

|

Role |

A network bridging the gap between the merchant and the bank. |

A solution streamlining end-to-end payment processes. |

|

Payment Options |

Primarily debit/credit card payments. |

Offers multiple options: UPI, debit/credit cards, net banking, etc. |

|

Integration |

Merchants integrate each payment method or bank separately. |

Integration requires partnering with just one service provider. |

|

Services Provided |

Transaction processing services. |

Provides transaction processing along with additional services like access to reports, customer support, etc. |

|

Funds Handling |

Does not store funds; securely transmits encrypted payment data. |

Handles funds through its Merchant Identification Number (MID). Transactions processed through the aggregator's system. |

|

Examples |

Axis Bank, HDFC Bank, MPGS (Mastercard Payment Gateways). |

PhonePe PG, Stripe, Cashfree. |

Payment and Settlement Systems (PSS) Act, 2007

- The Payment and Settlement Systems (PSS) Act, 2007, governs the supervision and regulation of payment systems in India. The Reserve Bank of India (RBI) is designated as the authority responsible for this and related matters.

- The Act empowers the RBI to form a committee within its Central Board called the Board for Regulation and Supervision of Payment and Settlement Systems (BPSS). This committee exercises the powers, performs the functions, and discharges the duties of the RBI under the statute.

- As per Section 4 of the PSS Act, 2007, only the RBI can authorize the operation of a payment system. Entities wishing to operate a payment system must apply for authorization under Section 5 of the PSS Act, 2007.

- The PSS Act 2007 does not prohibit foreign entities from operating a payment system in India. The Act ensures equal treatment and does not discriminate or differentiate between foreign and domestic entities.

- Operating a payment system without authorization, failing to comply with RBI directives, or violating any provisions of the PSS Act, 2007 can lead to criminal prosecution initiated by the RBI.

Must Check: Best IAS Coaching In Delhi

Indus Waters Treaty Under Climate and Security Stress

Echoes of Tyranny in Democracies

CJI Vows Transparency in Collegium Appointments

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.