- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- Answer Alpha: Mains 2025 Mentorship

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- Polity

- Geography

- Economy

- Ancient, Medieval and Art & Culture AMAC

- Modern India, Post Independence & World History

- Environment

- Governance

- Science & Technology

- International Relations and Internal Security

- Disaster Management

- Ethics

- NCERT Current Affairs

- Indian Society and Social Issue

- NCERT- Science and Technology

- NCERT - Geography

- NCERT - Ancient History

- NCERT- World History

- NCERT Modern History

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

NEW RULES AND REGULATIONS OF UPI: RBI

NEW RULES AND REGULATIONS OF UPI: RBI

In Jan 2024, the Reserve Bank of India (RBI) has announced new rules and regulations to enhance the scope of Unified Payments Interface (UPI) payments.

- Enhancing UPI transaction limit: The limit for UPI payments to hospitals and educational institutions has increased to Rs 5 lakh from Rs 1 lakh.

- Except for certain categories like Capital Markets, Collections, and Insurance, the general UPI transaction limit remains Rs 1 lakh, while it's Rs 2 lakhs for these specified categories.

- Increased e-Mandates for Recurring Online Transactions: The execution limit for e-mandates without Additional Factor of Authentication (AFA) has risen from Rs 15,000 to Rs 1 lakh.

- This limit has risen for credit card bill payments, mutual fund subscriptions, and insurance premiums.

- An e-Mandate is a digital payment service that allows businesses to collect recurring payments automatically without human interaction.

- An Additional Factor of Authentication (AFA) is a security process that requires users to provide two different authentication factors (like OTP) to verify themselves.

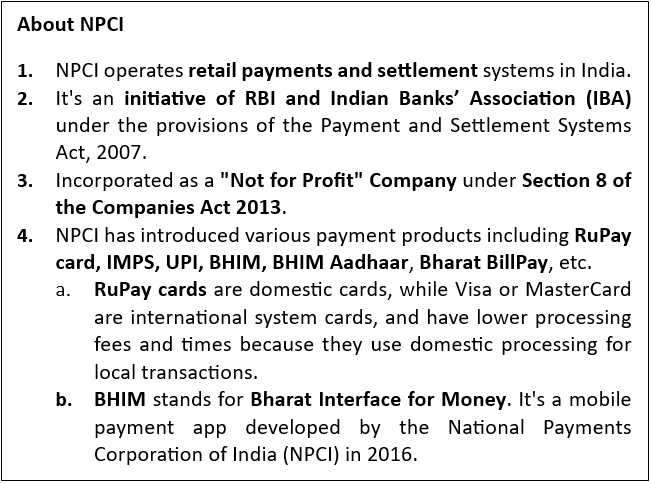

About UPI

- UPI consolidates multiple bank accounts into a single mobile application, offering various banking services like fund transfers.

- Developed by NPCI in 2016 over the Immediate Payment Service (IMPS) infrastructure.

- Immediate Payment Service (IMPS) is a service that allows users to transfer money instantly between banks in India. It is available 24/7, including on bank holidays.

- IMPS is facilitated by the National Payment Corporation of India (NPCI). It can be used through mobile phones, internet banking, or ATMs.

- It stands as the most successful real-time payment system globally, ensuring simplicity, safety, and security in person-to-person (P2P) and person-to-merchant (P2M) transactions in India.

New Features of UPI

- Credit Line on UPI: Now, banks can offer pre-approved credit lines through UPI, allowing transactions beyond deposited amounts. Earlier, only the deposited amount could be transacted through the UPI System.

- UPI Lite X: Enables offline money transfers using Near Field Communication (NFC) on compatible devices for both sending and receiving funds.

- NFC is a set of wireless technologies that allow two electronic devices to communicate within 4 centimeters of each other. It is a subset of radio-frequency identification (RFID), which uses radio waves to identify things.

- UPI Tap & Pay: Allows contactless payments at merchants using NFC-enabled QR codes, requiring just a single tap without PIN entry.

- Conversational Payments:

- Hello! UPI: Enables fund transfers through voice commands, followed by entering a UPI PIN for transaction completion.

- BillPay Connect: Customers can pay bills by sending a simple message or giving a missed call.

- Other Proposed Changes for UPI Payments:

- Deactivate UPI IDs: NPCI has instructed banks and mobile payment apps like Google Pay to deactivate UPI IDs and account numbers inactive for a year.

- Four-hour Time Limit: Users initiating first payments over Rs 2,000 to new recipients will have a four-hour window for UPI transactions, enhancing security and control.

- This allows users to reverse or modify transactions within that window.

- Introduction of UPI ATMs: Allows cash withdrawal by scanning a QR code, expanding UPI's utility.

Initiatives to Promote UPI

- UPI for Secondary Market: Introduced by NPCI to facilitate equity trading.

- UPI Chalega Campaign: NPCI's initiative to promote UPI as a safe, instant payment method and educate users about features like UPI LITE for swift low-value transactions.

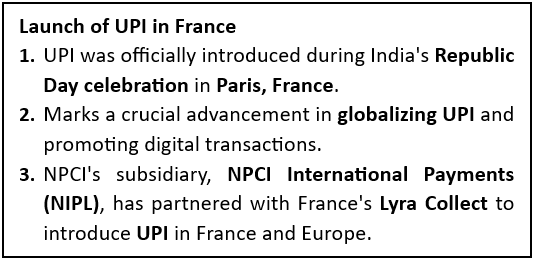

- MoU between Google India Digital Services and NPCI International Payments: Expanding UPI use for travellers abroad and easing remittance processes.

- India’s UPI in Overseas Markets: Several countries such as Oman, UAE, France, Nepal, and Bhutan have adopted the UPI system for payments.

- UPI 123PAY: An instant payment system for feature phone users, enabling them to use UPI services securely.

Benefits of UPI

Merchants |

Banks |

Customers |

Fintechs/PSPs |

|

|

|

|

Challenges and solutions

Challenges |

Solutions |

|

Expanding UPI globally requires compliance with various countries' data protection and financial laws, posing regulatory challenges. |

Collaborative efforts among nations and financial institutions are needed to establish a uniform regulatory framework. |

|

Cybercriminals can exploit system vulnerabilities or use social engineering to access sensitive information, leading to financial losses. |

Collaboration among UPI service providers, banks, and users is crucial to identify and address fraud incidents. |

|

Managing currency conversion and exchange rates for cross-border transactions poses significant challenges. |

Balancing security and transaction flexibility is essential to promote wider adoption of UPI across various sectors. |

|

Limited familiarity with digital payments among individuals hinders (hamper) UPI adoption and increases the risk of financial fraud. |

Training programs and user-friendly guides should be developed to educate people about the UPI ecosystem and address concerns. |

|

Dominance of foreign entities like PhonePe and Google Pay in the Indian fintech sector. PhonePe holds 46.91% market share, Google Pay has 36.39%, while BHIM UPI has only 0.22%. |

Banks and payment service providers must enhance their infrastructure to handle higher transaction volumes and accommodate global users and Indian fintech sector should make their infrastructure robust to compete. |

Must Check: Best IAS Coaching In Delhi

Green Hydrogen: High Hopes, Low Exports

Pulses & Oilseeds Crisis

PLACES IN NEWS 19th June 2025

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.