- Courses

- GS Full Course 1 Year

- GS Full Course 2 Year

- GS Full Course 3 Year

- GS Full Course Till Selection

- Answer Alpha: Mains 2025 Mentorship

- MEP (Mains Enrichment Programme) Data, Facts

- Essay Target – 150+ Marks

- Online Program

- GS Recorded Course

- Polity

- Geography

- Economy

- Ancient, Medieval and Art & Culture AMAC

- Modern India, Post Independence & World History

- Environment

- Governance

- Science & Technology

- International Relations and Internal Security

- Disaster Management

- Ethics

- NCERT Current Affairs

- Indian Society and Social Issue

- NCERT- Science and Technology

- NCERT - Geography

- NCERT - Ancient History

- NCERT- World History

- NCERT Modern History

- CSAT

- 5 LAYERED ARJUNA Mentorship

- Public Administration Optional

- ABOUT US

- OUR TOPPERS

- TEST SERIES

- FREE STUDY MATERIAL

- VIDEOS

- CONTACT US

Challenges Post GST Compensation Regime

Challenges Post GST Compensation Regime

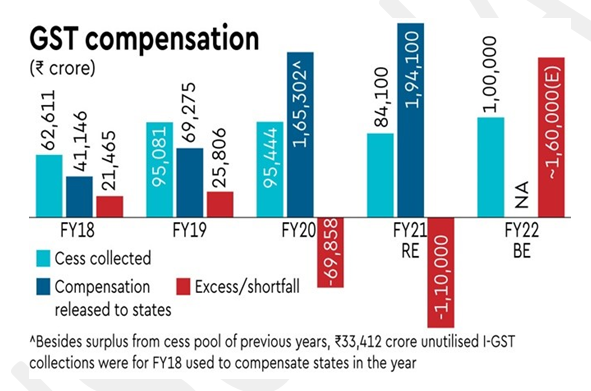

Latest Context

A significant transformation in India's taxation framework has taken place with the introduction of The Goods and Service Tax (GST). The implementation of the GST, however, raised concerns about potential revenue implications for those states which are known as manufacturing hubs. The Centre assured states the protection against revenue losses through GST compensation cess for a five-year period after the implementation of GST as a part of cooperative federalism. The Centre managed to clear outstanding dues through borrowings and expresses its commitment to assist the states even though the pandemic resulted in revenue dips for certain states. Till March 2026, this compensation cess was extended for the centre to regain the amount disbursed to states through the union exchequer. However, no state will be benefitted from the proceeds of the extended levy.

Fear of States with GST Regime

-

Absence of Role in Fixing the Tax Rate: Since the Centre has proposed a common tax for goods and services across the whole country therefore as per the states, they will not have any occasion and the authority to set tax rates on various items that could be highly detrimental fiscal federalism and their autonomy.

-

Revenue Distribution: The states that are well known for their production are in high fear that they will lose the opportunities for revenue generation in comparison to the "consumption states under the GST system. According to these states, they are producing more goods and selling them to less-developed states which will lead to comparatively less GST collection.

-

Revenue Loss: Transition from the previous tax regime to the GST system will lead to the potential loss of revenue because seventeen existing indirect taxes have been merged into one, it has become more crucial to know the "revenue-neutral" rate to secure that the same amount of revenue was collected as before. Inaccurate determination of the GST rate could lead to decreased revenue collection which will in turn increase the fiscal challenges.

Goods and Services Tax (GST)

- It is a value-added tax collected on almost all goods and services that are sold in the market for consumption. Under the GST, goods and services are taxed as per the place not the place where they originate. In other words, it is known as a destination-based tax.

- After the enactment of the 101st Constitution Amendment Act, 2016, the GST became applicable from 2017.

- Consumers are required to pay this tax but it is remitted to the government by the businesses selling the goods and services.

- Simultaneously, the Centre and the States levy tax on a common base. The tax collected by the Centre is known as Central GST (CGST) and in the case of States, it is known as State GST (SGST).

Measure that Encouraged States in GST Framework

-

Autonomy to Collect Revenue: Due to the permission given by the Centre to states for permitting them to have control over revenue from alcohol and petroleum products. These items have been kept out of the GST framework to make states capable to collect excise duty on alcohol and VAT on petroleum products. This kind of arrangement has proved very effective during the pandemic when tax collections plummeted.

-

Revenue Compensation: To deal with the concerns of the states regarding revenue collection, the Central Government made a commitment to the states of compensating any revenue loss under a growth rate of 14% (based on the 2015-16 baseline) for a period of five years. To fund this compensation, a compensation cess was introduced on luxury and sin goods.

-

Inclusion in the GST Council: To address the concerns of the states, the GST Council was created. It consists of each state’s representatives and the Union government which played a crucial role in gathering the support of states.

- It is the highest decision-making body for all GST-related matters that has voting provisions in the absence of consensus. The states collectively held two-thirds while The Union government held one-third of the votes. The purpose of the GST Council is to secure a cooperative and inclusive approach to decision-making.

Useful Measures for the States After the End of GST Compensation

States must find out alternative ways to increase their fiscal capacity when assured revenue protection comes to an end. It demands some proactive measures in order to maximize revenue collection while complying with the provisions of the GST.

-

Tailored Measures for Non-Compliant Taxpayers: On the basis of risk assessment and previous compliance history, states should make profile taxpayers. It will help in taking enforcement actions against the targeted persons or groups of persons effectively. This kind of strategy could be very useful in handling issues like circular trading and fraudulent invoicing.

-

Focus on the Service Industry: Due to having a right to levy GST on services, states must reassess its potential within their jurisdiction. Developing capacity and expertise in evaluating service-related transactions will widen the taxpayer horizon and will increase revenue collection. Additionally, there is a need on the part of states that should conduct GST audits and enhance the taxpayers’ awareness through trade facilitation kiosks and engagement programs.

-

Utilize Tax Analytics: To gain insights from comprehensive data analysis, states should adopt tax analytics strategies and processes. By taking the benefitted data collated from various sources, states can take informed decisions on the basis of accurate revenue projections.

-

Strengthen Compliance Monitoring: By cross-referencing e-way bill reports with data from road transport departments, states ought to reconcile information regarding the movement of goods. It assists in detecting potential discrepancies in addition to identifying non-compliant taxpayers. But, such comparisons ought to be judicious by considering variations arising from the different reporting requirements.

-

Foster Cooperative Federalism: All states ought to cooperate with each other by keeping the spirit of cooperative federalism in mind. States can create a business-friendly environment and foster taxpayer confidence by adhering to the principles of the GST laws and avoiding unnecessary territorial disputes. It will promote compliance, revenue boosting, and enhanced economic growth.

Conclusion:

There is a dire need on the part of the states to adapt as per the changing scenario of revenue generation. Although the Centre helped the States in the initial phase of GST implementation now the states have to cope with the challenges of increasing their revenue and widening the tax net. States can face these challenges successfully by employing proactive measures like strengthening compliance monitoring, leveraging tax analytics, emphasis on the service industry, and fostering cooperative federalism. States should create an environment that will catalyse the ease of doing business and inculcate confidence in taxpayers which will drive sustainable revenue growth and economic development.

Prelims

Q.1 Consider the following items: (2018)

1.Cereal grains hulled

2. Chicken eggs cooked

3. Fish processed and canned

4. Newspapers containing advertising material

Which of the above items is/are exempted under GST (Good and Services Tax)?

(a) 1 only

(b) 2 and 3 only

(c) 1, 2 and 4 only

(d) 1, 2, 3 and 4

Ans: (c)

Q.2 What is/are the most likely advantages of implementing ‘Goods and Services Tax (GST)’? (2017)

1. It will replace multiple taxes collected by multiple authorities and will thus create a single market in India.

2. It will drastically reduce the ‘Current Account Deficit’ of India and will enable it to increase its foreign exchange reserves.

3. It will enormously increase the growth and size of economy of India and will enable it to overtake China in the near future.

Select the correct answer using the code given below:

(a) 1 only

(b) 2 and 3 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: (a)

Mains

Q:1 Explain the salient features of the Constitution (One Hundred and First Amendment) Act, 2016. Do you think it is efficacious enough “to remove cascading effect of taxes and provide for common national market for goods and services”? (2017)

Q:2 Explain the rationale behind the Goods and Services Tax (Compensation to States) Act of 2017. How has COVID-19 impacted the GST compensation fund and created new federal tensions? (2020)

Q:3 Enumerate the indirect taxes which have been subsumed in the Goods and Services Tax (GST) in India. Also, comment on the revenue implications of the GST introduced in India since July 2017. (2019)

Must Check: Best IAS Coaching Centre In Delhi

Indus Waters Treaty Under Climate and Security Stress

Echoes of Tyranny in Democracies

CJI Vows Transparency in Collegium Appointments

Karol Bagh Metro Pillar No. 112, Above Domino's, 22B, First Floor, New Delhi - 110060

Very Important Instruction For Any Issue, Student Must Produce His/Her Fee Receipt. Without Fee Receipt, It Will Not Be Possible To Track Your Details. If You Have Been Given Any Special Consideration, You Must Keep That In Writing And Produce In Case Of Conflict.

Copyright © 2024-2026 ENSURE IAS. All rights reserved.